Roof Shingles Depreciation

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

N C High Court Actual Cash Value Includes Depreciation For Labor Costs

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Roof Insurance Acv Vs Replacement Cost Bankrate

Roof Deductible L Depreciation L Roof Insurance Claim Specialists Bbr Contracting Residential Commercial Roofing Services

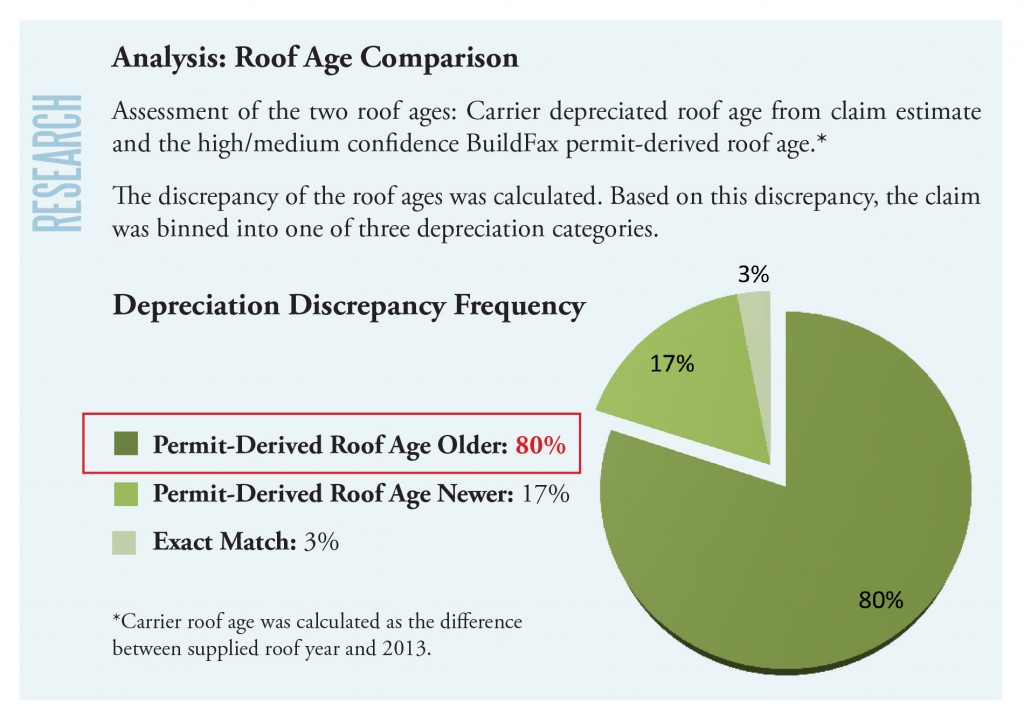

This loss in value known as depreciation can significantly affect the amount that a policyholder is paid for a claim.

Roof shingles depreciation.

Home Insurance And Roof Schedules

How To Understand Depreciation On Your Roof Insurance Claim

Guide To Expensing Roofs Expense V Capitalization Section 179 D Kbkg

Part Three The Value Of Accurate Roof Age In Claims

Depreciating Labor Costs The Rough Notes Company Inc

Roof Insurance Claim Denied

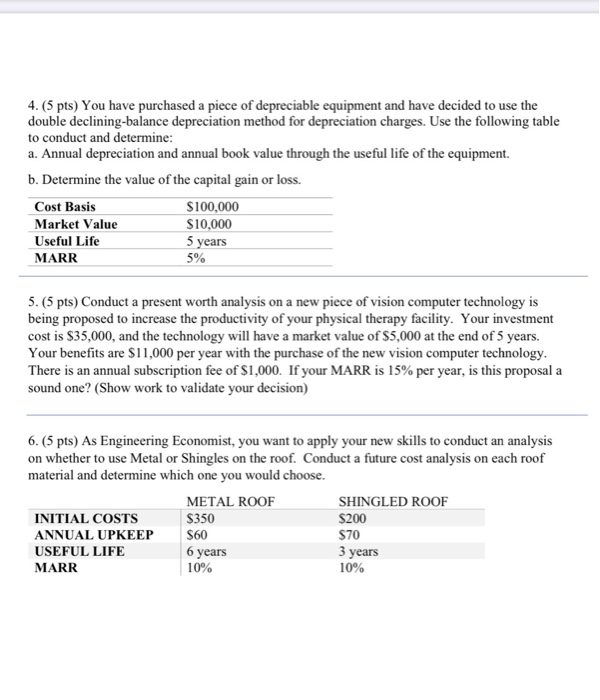

Solved 4 5 Pts You Have Purchased A Piece Of Depreciab Chegg Com

Https Www Milestonepnc Com Wp Content Uploads 2017 12 Acv Loss Settlement Wind Hail Losses Mic Ho Tx 1014 08 15 Maison Insurance Pdf

Roof Damage And Replacement Block S Agencies Block S Agencies

Is It Legal For A Roofer To Cover My Insurance Deductible

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

Homeowners Insurance 101 Roof Age Matters At Claim Time

How To Get Your Homeowners Insurance To Pay For A New Roof Clever Real Estate Blog

How To Make A Home Insurance Claim For Roof Damage Forbes Advisor

Are Asphalt Shingles Any Good Ats Exteriors

Top Roofing Materials That Boast High Wind Resistance

How I Do Business Kat Constructions Llc

How To Get Insurance To Pay For Your Roof Replacement In 2020

Roofing Tegola Master Everything On A Single Roof These Are The Characteristics Of Any Tegola Canadese Roof Quali Shingling Building Shingles Roof Shingles

Frequently Asked Questions High Performance Restoration

What Is The Depreciation Of The Roof On A Commercial Building

T Lock Shingles Your Secret Upper Hand Ropa Roofing

Section 179d Tax Deduction For Commercial Roof Replacements

Interpretation Of Actual Cash Value In Mississippi Property Insurance Coverage Law Blog Merlin Law Group

Source : pinterest.com