Roof Replacement Repair Or Depreciate

How To Get Insurance To Pay For Roof Replacement Rgb Construction

Looking For A New Roof Here Are The Tips Copper Gutters Craftsman Exterior Copper Roof

Section 179d Tax Deduction For Commercial Roof Replacements

Guide To Expensing Roofs Expense V Capitalization Section 179 D Kbkg

Are Roof Repairs Tax Deductible The Roof Doctor

How To Get Your Homeowners Insurance To Pay For Roof Replacement

In many cases only a portion of the roofing system is replaced and depending on the facts those costs may be deducted as repairs.

Roof replacement repair or depreciate.

Tips For Filing A Roofing Insurance Claim With Images Roofing

What Is The Depreciation Of The Roof On A Commercial Building

Seeking Knowledge About Roofing You Need To Read This Article Roof Repair Bathroom Fan Roof

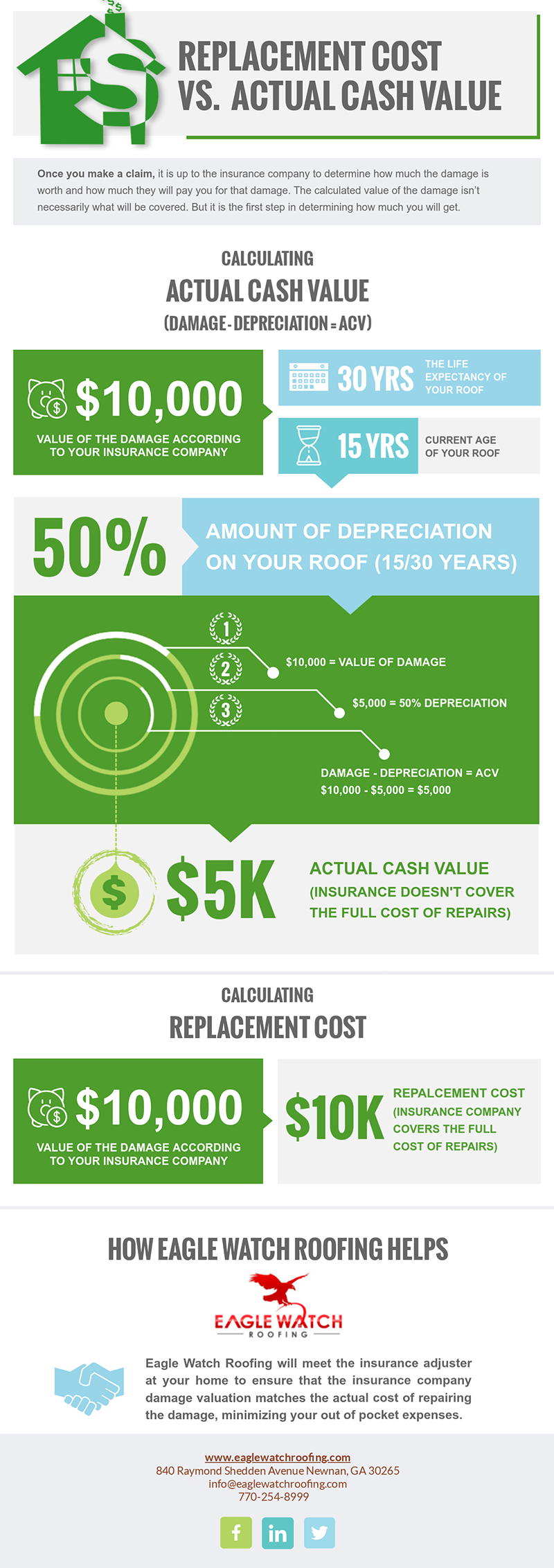

Rcv Vs Acv Policies Premier Claims

4 Things You Need To Know About Roof Replacement Deductibles Patriot Roofing Llc

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

5 Ways Not To Save Money On Homeowners Insurance Homeowners Insurance Saving Money Homeowner

Pin On Articles Tips

Reasons For The Awning Getting Torn And Rv Awning Repair In This Case Rv Travel Trailer Rvs Campers Tenttrai Camper Awnings Rv Awning Fabric Rv Lighting

A Frequently Asked Question We Get Is Are Copper Gutters Worth The Investment The Answer Is While They Can Last Longer Than Traditio Copper Gutters Copper House Copper Roof

Repairing Damaged Gutters Gutter Repair Home Repairs Home Repair

How To Understand Depreciation On Your Roof Insurance Claim

Pin On Roof Repair

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Do Double Wide Mobile Homes On A Full Concrete Foundation Depreciate Mobile Home Doublewide Single Wide Mobile Homes Clayton Modular Homes

Replacement Cost Vs Actual Cash Value Eagle Watch Roofing Atlanta Georgia

Replacing Your Roof With An Insurance Claim

Roof Insurance Acv Vs Replacement Cost Bankrate

Sample Roofing Contract Free Printable Documents Roofing Contract Contract Template Roofing

Homeowners Insurance 101 Roof Age Matters At Claim Time

My Heart S Song Mobile Home Exterior Before After Remodeling Mobile Homes Mobile Home Exteriors Manufactured Home Remodel

How To Get Your Homeowners Insurance To Pay For A New Roof Clever Real Estate Blog

Replacing Rotten Floor Joists Google Search Mobile Home Renovations Repair Floors Mobile Home

Filing An Insurance Claim How You Get Paid Do You Know What Acv Or Rcv Means If Not Here S Some Helpful Informa Roofing Insurance Claim General Contracting

Source : pinterest.com